Framework: Unit Economics

Category: Frameworks

Core Question: When does growth strengthen a business, and when does it merely scale activity?

Objective: Teach readers how Unit Economics helps separate real value creation from surface growth across different business models.

Growth is one of the most misread signals in investing.

That is partly because growth feels intuitive. More customers, more revenue, more locations, more product adoption, and more volume all sound like obvious signs of strength.

But serious investors eventually learn that growth is not the same thing as value creation. A business can grow while becoming stronger, or it can grow while becoming more fragile, more expensive, or more complicated.

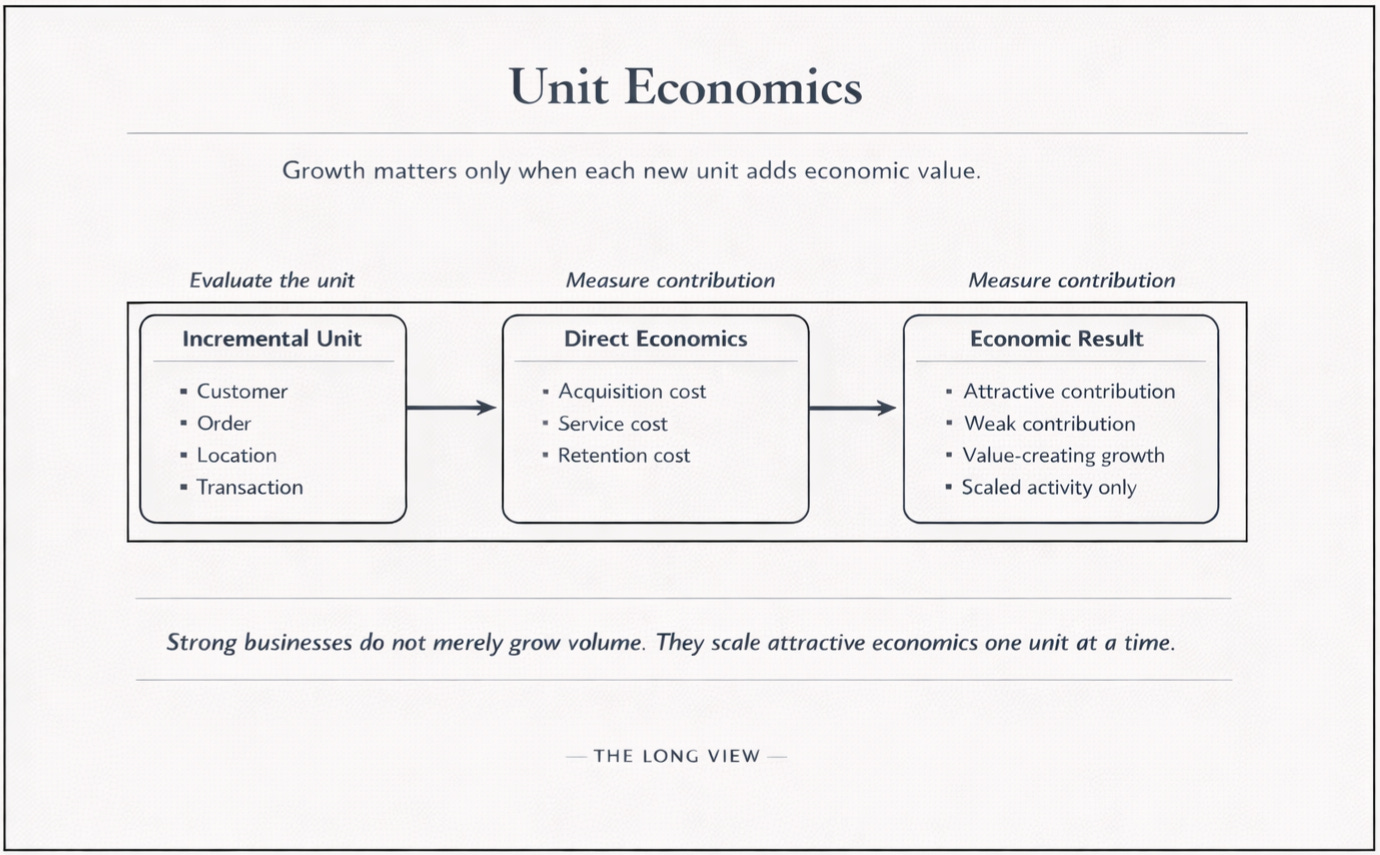

That is why Unit Economics matters.

Unit Economics asks whether each additional unit — a customer, order, store visit, vehicle, seat, workflow, or relationship — creates attractive value after the direct costs required to win, serve, and retain that unit are considered.

This framework pulls the reader away from surface expansion and back toward the thing that actually matters:

Is the business earning enough on each incremental unit to make growth worthwhile?

This week’s four companies show why that distinction matters.

Ferrari is the cleanest case because it breaks the common assumption that better businesses should always maximize units. Ferrari does not organize the business around selling as many vehicles as possible. It organizes the business around maximizing the value of each vehicle through scarcity, product mix, pricing, and brand strength.

That makes it a powerful reminder that excellent Unit Economics can come from control and selectivity, not just scale.

Aptiv is the harder case.

Here, the surface story can sound attractive quickly. More embedded content, more software, and more systems complexity can all sound like automatic evidence of better economics. But Unit Economics forces the reader to slow down.

More complexity is only valuable if the incremental economics justify it.

A business can deepen its technical role while weakening its economic returns if cost, execution burden, or fragility rise faster than value.

Home Depot brings the framework into large-scale retail.

The company is useful because its units are visible. Investors can think in terms of stores, visits, baskets, categories, and professional customer relationships. That makes the framework easy to see.

But the lesson is deeper than visibility.

Home Depot shows that scale is not quality by itself. A large retail system only deserves respect if the underlying units remain productive. A store base can expand. Traffic can rise. Sales can grow. None of that settles the question unless the economics of those units remain attractive.

Atlassian extends the same logic into software.

In this case, the units are seats, workflows, adoption, and expansion inside the customer base. The business can appear strong because software growth often looks clean from the outside. But software is not exempt from the framework.

More seats and more product usage only matter if the economics of customer expansion remain attractive.

The company helps show that Unit Economics is not a retail idea, a software idea, or a luxury idea.

It is a business-quality idea.

Taken together, the four companies reveal a deeper pattern:

Ferrari represents economics deepened by scarcity and pricing.

Aptiv represents economics tested by complexity.

Home Depot represents economics made visible through productivity at scale.

Atlassian represents economics expressed through expansion inside a software platform.

The industries differ.

The units differ.

The framework does not.

That is the real value of Unit Economics.

It trains the investor to stop asking whether a business is growing and start asking whether the growth is worth having.

That shift sounds small, but it changes the quality of judgment dramatically.

It forces attention toward cost to serve, pricing power, operating leverage, customer quality, retention, expansion, and the relationship between incremental growth and incremental value.

It also protects against one of the easiest investing mistakes: rewarding motion without understanding economics.

The market often gives surface growth too much credit, especially when the story is easy to narrate. But stronger investors eventually learn that motion is not enough.

They want to know whether the next unit is productive, whether it strengthens the system, and whether the business earns enough on that growth to make it meaningful.

Evaluation Checklist

What is the actual unit in this business?

What does it cost to acquire, serve, and retain that unit?

Does each additional unit deepen value creation or just increase activity?

Is growth improving the economics, or simply scaling the system?

What would weaken the economics of the next unit?

The practical lesson is durable:

Growth should not be treated as proof. It should be treated as a question.

When a reader begins to think that way, they stop reacting to expansion as an automatic positive and begin judging whether the business underneath the growth is actually getting stronger.

That is a better habit, a better discipline, and usually the beginning of better investing.

Postscript

The full Long View Institutional Review for Home Depot is available to paid subscribers in the Review System archive. The Price / Value companion accompanies this week’s archive entry.

Memo Companion Note

The market often rewards visible growth first and asks harder questions later.

Unit Economics reverses that order.

It asks whether the next customer, next seat, next basket, or next vehicle is worth having before it rewards the growth itself.

That is a stronger way to judge business quality.