The Dividend King That Keeps Going on Sale

Cincinnati Financial has raised its dividend for 65 straight years. It has also handed patient buyers a bargain over and over. Those two facts are connected, and the reason why is worth understanding.

I own this stock. I have bought it several times over the years, and I have never once bought it at its high. That is not because I am a good market timer. I am not. It is because Cincinnati Financial keeps offering the same gift, if you know what to wait for.

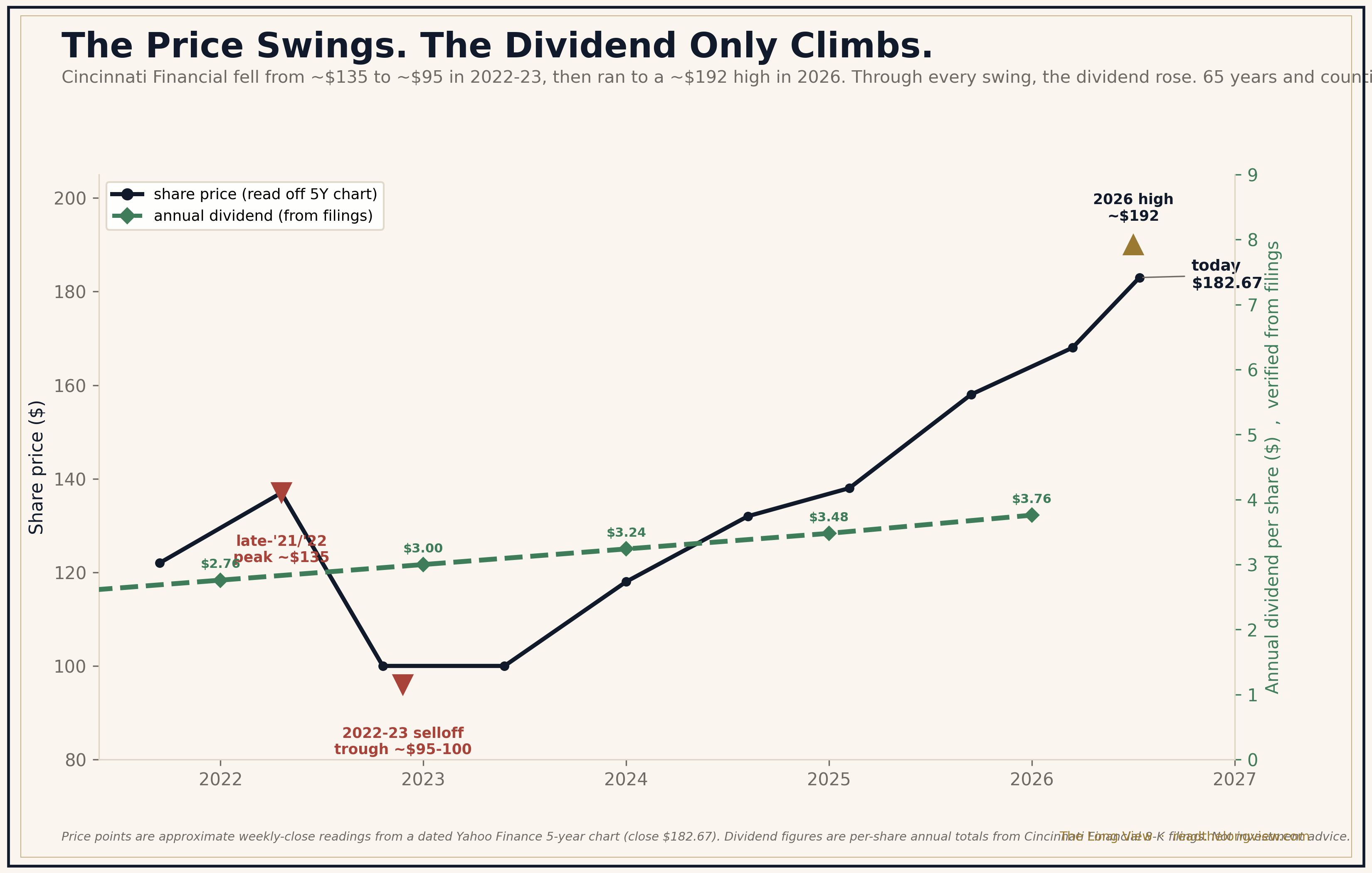

Here is the pattern. The stock runs up, looks expensive, and everyone loses interest at exactly the wrong moment. Then the market has a bad stretch, the price falls back, and there is the entry again. Through every one of those dips, the dividend did not just hold. It rose. Sixty-five years in a row, without a single miss, through recessions, a pandemic, and more than one market crash.

CINF’s share price swung from about $135 to about $95 in 2022-23, then ran to a ~$192 high in 2026, while the dividend rose every year.

Most people see the 65-year streak and assume it means the stock never gets cheap. The opposite is true. The streak and the bargains come from the same place.

Why a great company keeps going on sale

Cincinnati Financial is an insurer, but it does not behave like most insurers, and this is the key. It keeps roughly 40 percent of its investment portfolio in common stocks, an unusually large equity book for a company in its business.

That single fact explains the whole pattern. When the stock market falls, the value of that equity portfolio falls with it. That drags down Cincinnati’s reported book value and its reported earnings, even in a quarter where the actual insurance business, the underwriting, is running exactly as well as before. The headline number looks worse. The stock sells off. And the people watching only the headline walk away.

But the dividend is not paid out of that equity portfolio’s paper value. It is paid out of the underwriting profit and the steady investment income underneath. So the thing that scares people out of the stock, a market drawdown, is not the thing that pays the dividend. The engine keeps running while the price falls.

That is the gift. The bargain in Cincinnati Financial is almost never created by the insurance business breaking. It is created by the stock market having a bad day and taking Cincinnati’s share price down with it, while the business itself keeps compounding.

What this means if you own it for income

If you are buying Cincinnati for price appreciation, the current price near its all-time high is not attractive. We said as much in our full breakdown of the company.

But if you are buying it for income, for a dividend that has risen every year for two-thirds of a century, the question is different. You are not trying to catch the bottom. You are waiting for one of the recurring dips, the ones the market hands out every few years, to start a position or add to one at a better yield. History says you will not have to wait long, and history says the dividend will keep climbing while you do.

That is not a prediction. Past bargains do not guarantee future ones. But the mechanism that created them, a market-sensitive equity portfolio bolted onto a disciplined insurer, has not changed. As long as it is there, the pattern has a reason to keep repeating.

The streak tells you the dividend is durable. The equity portfolio tells you the price will keep giving you chances to buy it. Patience, not timing, is the whole strategy.

The author holds shares of CINF, bought over time and never at the high. This is a disclosure, not a recommendation. Our full earnings analysis of Cincinnati Financial, including the test we set for its next print, is available separately.

Not investment advice. The subscriber decides.