Spotify added 252 million paid subscribers last year.

The stock rewarded them for it.

But here is the question nobody asked loudly enough:

Is Spotify becoming more valuable because more people use it — or because each layer of use is becoming more economically productive?

Those are not the same claim.

And the distance between them is where investors lose money.

This is not a memo about whether these businesses are good.

Spotify is real. Brown-Forman is real. NextEra is real. Toyota is real.

The demand is visible. The revenue is there. The headlines are supportive.

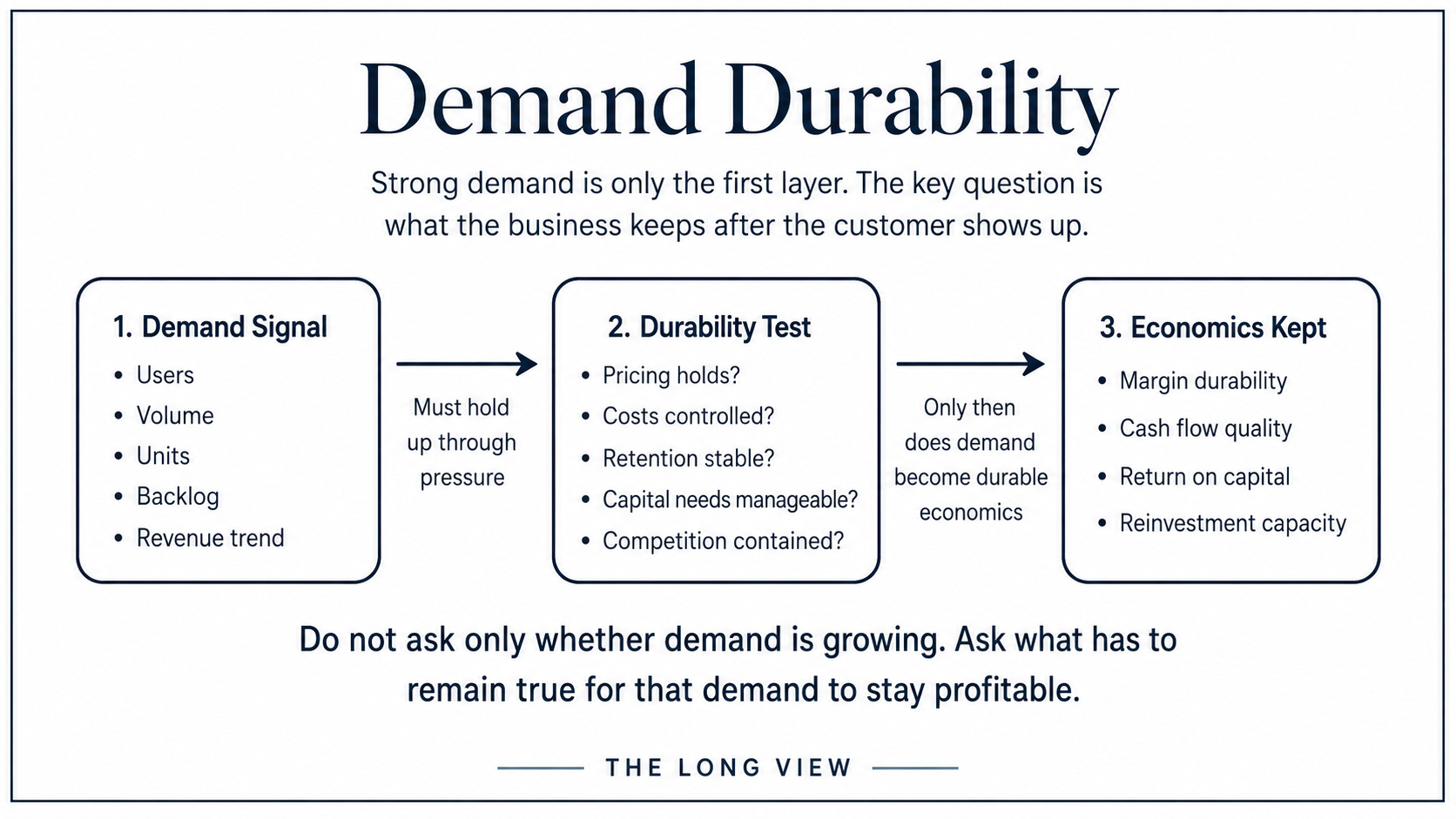

But demand is not one signal. It is a chain.

At one end: the thing you can see. Users. Volume. Units. Backlog. Revenue.

At the other end: the thing that actually matters. Margin. Pricing power. Free cash flow. Returns on capital. Resilience when conditions stop being forgiving.

The danger is not at either end.

The danger is in the space between them — the part investors skip.

A good quarter proves customers showed up.

It does not prove the company can keep converting that arrival into attractive economics. Not when competition tightens. Not when rates stay higher. Not when the category softens. Not when the tariff lands.

That is the distinction this week is built around.

And it is why four very different companies belong in the same analysis.

Because demand fails in different ways. Each business has a different link in the chain that breaks first. Understanding which link is the entire job.

Spotify — The Monetization Gap

The audience is not the moat.

This is the most important sentence you will read about Spotify, and it contradicts the way most investors talk about the company.

Scale creates the opportunity. Monetization quality determines whether the opportunity compounds. Those are sequential — not simultaneous. Investors consistently price them as if they arrive together. They do not.

Spotify has 268 million paid subscribers. Monthly active users approaching 700 million. Engagement metrics that most platforms would trade their entire product roadmap to own. If you stopped the analysis there — and many investors do — you would conclude the business is working exactly as designed.

It is. Just not in the way the stock needs it to work yet.

The framework question is not: are people listening?

The world already answered that.

The question is: is listening becoming more valuable?

That requires something harder than audience growth. It requires paid conversion improving — the rate at which free users become paying subscribers. It requires pricing power in a market where Apple Music, YouTube Music, and Amazon Prime Audio are credible alternatives. It requires advertising economics that hold when the digital ad cycle softens. It requires content costs — podcasts, audiobooks, licensing — that remain disciplined as the platform expands into more formats. It requires operating leverage: revenue growing faster than the cost structure.

Spotify has shown genuine progress on operating leverage. Gross margins are expanding. The business is moving toward profitability in a way that was not obvious two years ago.

But here is the second-layer pressure: Spotify’s pricing power is structurally constrained by the music labels. Approximately 70% of revenue flows back to rights holders before Spotify gets to report a gross margin. When Spotify raises prices — as it has, in multiple markets — it does not keep the full incremental dollar. The labels capture a significant share of any ARPU improvement through their revenue-sharing agreements.

That is not a fatal flaw. It is a structural ceiling on how fast Spotify’s economics can improve relative to its revenue growth.

What has to remain true for Spotify’s demand to stay profitable: Paid conversion must keep improving. Advertising must hold through the cycle. Pricing increases must flow through to net revenue faster than label costs reprice. The podcast and audiobook bets must generate revenue dense enough to justify their cost without label exposure.

If the audience grows and none of those conditions hold — the demand signal was real and the economic return was not.

That is the Spotify risk. Not that the platform fails. That it succeeds at a scale the economics cannot adequately reward.

Brown-Forman — The Brand Trap

Brand strength and demand durability are not the same thing.

This is the slower version of the Spotify mistake — and it is more dangerous, because the evidence arrives later.

Jack Daniel’s is one of the most recognized spirits brands on the planet. Woodford Reserve helped define the American whiskey renaissance. Herradura anchors premium tequila. Old Forester is a legitimate craft story. The distribution network is deep. The shelf presence is real. The pricing history is long.

Every surface indicator says the business is protected.

But surface indicators are exactly what you should distrust when analyzing a consumer brand. The surface can remain intact long after the economics underneath begin to erode. The bottle stays on the shelf. The brand stays famous. The company still has pricing history. And meanwhile — volume softens, occasions shrink, younger consumers enter differently, GLP-1 medications reshape discretionary spending habits, and the premium spirits category that once felt invincible begins to bifurcate between genuine luxury and challenged aspirational.

Brown-Forman is not in crisis. That framing would be wrong and lazy.

What it is facing is something quieter and harder to model: slow category erosion beneath sustained brand equity. The brand is not breaking. The demand structure attached to the brand is becoming less forgiving.

Consider what happened to volume. American whiskey had a decade of exceptional tailwinds — craft culture, premiumization, the global appetite for American goods, a generation discovering bourbon. Those tailwinds made Brown-Forman’s economics look better than they structurally were. Pricing lifted easily. Volume held. Margins expanded.

When tailwinds become headwinds — or even just neutral — brands do not always have the pricing power investors assumed. The loyalty is real but conditional. The consumer who paid $45 for Woodford will consider a $38 alternative if the category has lost some of its cultural urgency.

This is slow erosion. It does not announce itself loudly. It shows up through guidance that keeps getting trimmed, organic growth that keeps disappointing slightly, volume that keeps running below volume expectations. The numbers are not catastrophic — they are persistently softer than the brand equity would suggest.

What has to remain true for Brown-Forman’s demand to stay profitable: Volume must recover in core markets, particularly the US. Pricing must hold without accelerating trade-down to value alternatives. The premium tequila segment must grow fast enough to offset American whiskey pressure. International markets — particularly the EU — must not face sustained tariff headwinds. And GLP-1 behavioral effects on alcohol consumption must remain a research question rather than a confirmed structural shift.

If those conditions loosen — the brand will remain valuable and the returns will become harder to compound.

That is the Brown-Forman risk. Not collapse. Compression.

Slow enough that most investors won’t notice until three years of slightly disappointing results have already happened. Which, for many investors, is the worst possible outcome.

NextEra Energy — The Capital Conversion Problem

The demand story is not the question.

Data centers need power. Electrification needs power. Reshoring of manufacturing needs power. Grid modernization needs power. Renewable energy needs capital. Storage needs capital. Transmission needs capital.

All of that is real. The policy tailwinds are real. The industrial trends are real. The secular direction of electricity demand is not seriously in dispute.

But demand and shareholder return are not the same thing inside a capital-intensive infrastructure business.

This is the link in the chain most investors miss with utilities.

A software company can serve incremental demand with extremely high incremental margins. The cost of the next user is close to zero. The economics of scale are nearly automatic.

A utility cannot do this.

NextEra has to turn demand into approved projects. Approved projects into permitted construction. Permitted construction into completed assets. Completed assets into rate base or contracted revenue. Contracted revenue into regulated or contracted returns. And those returns must exceed the cost of the capital deployed — which, in a higher-rate environment, is no longer trivially cheap.

Every link in that chain can slow, reprice, or break.

Interconnection queues for new renewable projects have become severe. Permitting timelines have extended. Construction costs have risen with inflation and tariffs on imported materials. The interest expense on the debt used to finance new builds has increased meaningfully. And the customer affordability pressure — the utility commission’s obligation to keep rates reasonable for residential and commercial customers — constrains how much of the cost increase NextEra can pass through.

This is not a verdict that NextEra is a bad business. It is a sophisticated, well-run infrastructure platform.

It is a verdict that the market price has frequently reflected a future in which demand converts to shareholder return cleanly. That conversion is more expensive, slower, and more uncertain than the headline demand narrative implies.

What has to remain true for NextEra’s demand to stay profitable: Interest rates must not continue rising, because each point of rate increase degrades the economics of the next project. Interconnection queues must clear at a pace that allows contracted backlog to convert to earning assets on schedule. Regulatory commissions must allow sufficient cost recovery. Tariffs on solar panels and construction materials must not structurally impair project returns. And the cost of equity must remain low enough to justify continued capital deployment at scale.

The demand is real. Whether it earns an attractive return for shareholders depends on conditions that are genuinely uncertain in 2026.

That is the NextEra risk. Visible demand. Expensive conversion.

Toyota — The Profit Conversion Problem

The car will sell.

That is not the question.

Toyota is the most efficient large-scale automaker in the world. The production system is the standard. The hybrid technology is a decade ahead of most competitors in commercial deployment. The brand credibility — particularly in reliability — is real and hard-won.

Global vehicle demand will not collapse. Toyota will sell cars.

But here is what the auto industry has always taught patient investors: customer demand and investor economics can separate quickly, and they can stay separated for a long time.

The unit sells while the margin weakens.

Consider the compression points Toyota faces simultaneously: Tariffs on vehicles exported from Japan to the US, its most profitable market. Currency movements that make yen-priced costs expensive when translated into dollar revenues. Raw material and supplier input costs that remain elevated. Incentive spending that has increased across the industry as competition for market share intensifies — particularly against Chinese manufacturers expanding globally at aggressive price points. Transition spending on battery EVs that Toyota must fund even as its hybrid business funds those investments. And regional mix shifts, as some of Toyota’s highest-margin markets are growing more slowly than its lower-margin markets.

None of these individually breaks Toyota.

All of them together compress operating margins in a way that makes the demand story look better than the earnings story.

The customer still wants the car. The question is what Toyota keeps after building it, sourcing it, shipping it, financing it, and competing globally to sell it.

That answer is not obvious. And it is not answered by looking at unit volumes.

What has to remain true for Toyota’s demand to stay profitable: Tariff headwinds must not structurally reprice North American economics. The yen must not strengthen against the dollar faster than Toyota can reprice or hedge. Hybrid demand must remain strong enough in the US and Europe to sustain premium margins while the full EV transition remains uncertain. Chinese competition must not accelerate into Toyota’s core markets faster than pricing power allows Toyota to hold.

The demand is there. Whether the margin follows is the entire question.

The Transferable Lesson

Four different businesses. Four different failure modes.

Spotify: monetization quality. The audience is real; whether listening keeps converting into economics is not yet proven.

Brown-Forman: category erosion beneath brand strength. The brand is real; whether the demand structure attached to it remains healthy is what erodes slowly and quietly.

NextEra: capital conversion cost. The end-market demand is real; whether it passes through a long capital chain with adequate returns is genuinely uncertain.

Toyota: profit conversion. The product demand is real; whether the margin survives the journey from customer to shareholder is where the business can quietly disappoint.

The mistake is not believing in the demand.

The mistake is assuming the demand already answers the harder questions.

The question to carry into every earnings season:

What has to remain true for this demand to stay profitable?

Not: is demand growing?

Not: are revenues increasing?

Not: is the backlog healthy?

What has to remain true — in the cost structure, the competitive environment, the capital markets, the regulatory framework, the consumer behavior — for this demand to keep converting into the economics the stock needs.

That is where the real analysis begins.

That is where most analysis stops.

The Long View memo is published weekly for self-directed investors who want understand frameworks, not forecasts.