Reinvestment Runway: Why a Strong Business Is Not Always a Long-Duration Compounder

How long can a business keep deploying capital at attractive returns? That question matters more than most investors realize.

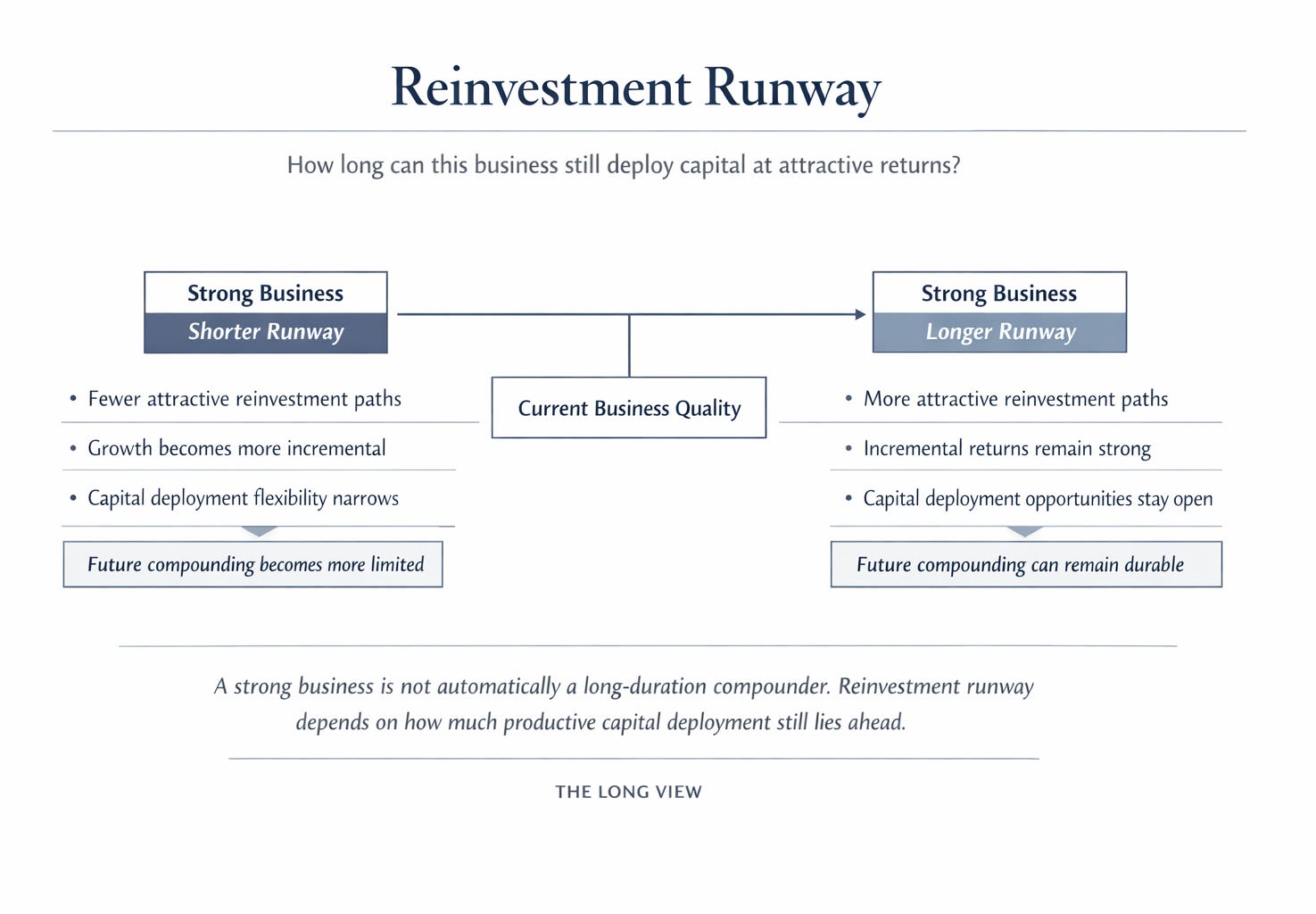

Many companies deserve to be called high quality. They may have strong margins, loyal customers, durable demand, pricing power, or respected management teams. But quality alone does not guarantee long-term compounding.

What ultimately separates a good business from a great long‑duration compounder is something subtler:

How much productive opportunity still lies ahead?

That is what the Reinvestment Runway framework is designed to answer.

The Core Idea: Quality vs. Compounding Depth

A strong business is not automatically a long‑term compounder.

This is one of the most important distinctions in serious investing, and one of the easiest to miss. Investors often learn to recognize quality before they learn to ask the next, harder question:

Can this business keep reinvesting capital at attractive returns for many years to come?

Future investment returns are shaped by more than today’s business quality. They are shaped by:

How long reinvestment opportunities remain available

Whether those opportunities stay attractive as scale increases

Whether returns on incremental capital deteriorate over time

Professional investors tend to be more cautious here. They don’t just admire great businesses—they underwrite future capital deployment.

That difference matters.

What “Reinvestment Runway” Really Measures

Reinvestment Runway asks a stricter question than moat or quality analysis:

How much capital can this business still put to work at strong returns without the economics getting worse?

Some businesses are excellent at defending what they already have.

Others are exceptional because they can still build at high returns for a very long time.

That second group is rarer—and far more powerful for long-term compounding.

Four Businesses, Four Different Runways

Looking at real companies makes the framework clearer.

Diageo: High Quality, Bounded Opportunity

Diageo is undeniably a strong business. Its brands are durable, its global reach is unmatched, and it has meaningful pricing power.

But Reinvestment Runway asks a tougher follow‑up:

After brand support

After portfolio management

After selective geographic expansion

How much attractive future deployment remains?

Diageo shows that a business can be excellent without having an unusually open‑ended reinvestment path.

National Grid: Scale Without Flexibility

National Grid illustrates a different lesson.

The company can clearly deploy large amounts of capital over time. Its assets are durable, regulated, and tied to essential infrastructure.

But scale alone doesn’t answer the framework question.

The key issue is the quality and flexibility of reinvestment, not just its size. National Grid demonstrates that:

Large reinvestment needs do not automatically imply high returns

Bounded economics can limit compounding even when capital deployment is ongoing

Dollar General: The Narrowing Middle Case

Middle cases are where frameworks become most useful.

Dollar General still has visible growth opportunities. But visible growth is not the same as attractive incremental reinvestment.

The key question becomes:

Does the next phase of growth look as good as the earlier one?

Dollar General shows how a reinvestment runway can remain real while also becoming:

More incremental

More operationally demanding

Less forgiving over time

This is often how strong businesses mature.

HDFC Bank: Quality and Opportunity Aligned

HDFC Bank is the strongest example in the group.

In financials, Reinvestment Runway must be applied carefully—but the principle still holds. When:

Underwriting discipline

Distribution strength

Market opportunity

remain aligned, a business can keep deploying capital productively for a long time.

HDFC Bank illustrates what a deep reinvestment runway looks like when business quality and future opportunity reinforce each other rather than trade off.

What the Framework Is Not Saying

Reinvestment Runway is not about labeling companies as “good” or “bad.”

It is about understanding that:

Strong businesses do not all compound in the same way

Growth alone is not enough

Future returns depend on tomorrow’s opportunity set, not just today’s strength

This is why two high‑quality companies can deserve very different long‑term expectations.

A Simple Evaluation Checklist

When analyzing a business, ask:

Does the business still have meaningful future uses for capital?

Are those uses likely to earn attractive returns?

Is the opportunity set broad—or becoming more incremental?

Does growth strengthen the compounding engine or slowly narrow it?

Is management capable of allocating capital well as the business matures?

The Long View

The takeaway is simple:

Do not confuse business quality with future compounding depth.

A strong business may still be worth owning, studying, or admiring. But the best long‑term compounders are the businesses that still have somewhere productive to put capital for many years to come.

That is why Reinvestment Runway matters—and why understanding it makes professional investing language much easier to decode.