Pepsi Says It’s the Economy. Coke’s Shoppers Didn’t Get the Message.

The Firewall named Pepsi’s bet in June: that its brands can charge more than the store brand and keep the customer.

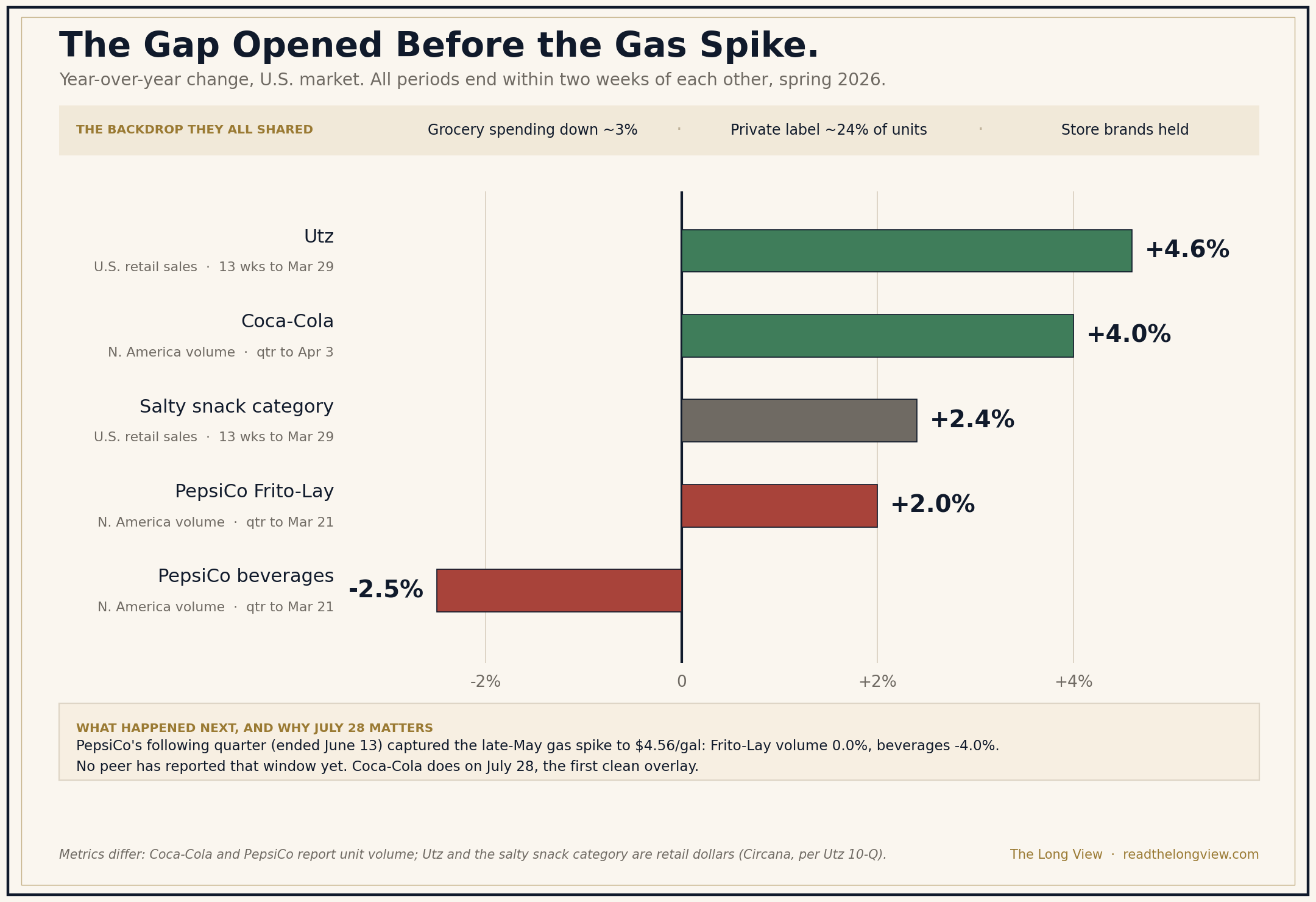

Stand in the chip aisle for a second.

It’s February. Lay’s, Doritos, Cheetos and Tostitos have all gotten cheaper, some by as much as 15 percent. Pepsi cut those prices on purpose, to win you back after two years of trading down to the store brand.

Thursday we found out what you did. North America food volume for the quarter: flat. North America beverage volume: down 4 percent.

The price came down. The shoppers stayed where they were.

The easy read is that Pepsi’s moat is cracking. But there’s a harder question underneath, and it’s the one that decides whether this quarter means anything.

Give the economy its due, because the case is strong

Every American shopper is being squeezed right now, and Pepsi did not cause that.

Gas hit a four-year high of $4.56 a gallon in late May on oil swings from the war with Iran. Consumer Edge data shows U.S. grocery spending down roughly 3 percent year over year. Ramon Laguarta wrote that results were “tempered” as U.S. category performance moderated with consumer budgets tightening.

That is not spin. It is a description of the country. If the shopper in the chip aisle just watched forty dollars leave her tank, the Doritos lose whether or not Frito-Lay has a moat.

So the question is not whether Pepsi’s volume fell. It’s whether it fell more than the economy explains. Macro pressure and moat erosion look identical from inside one income statement. You cannot separate them without looking outside it.

What the tool told us to look for, back in June

When we ran PepsiCo through the Stock Story Firewall on June 25, it named the assumption the share price rests on: that PepsiCo’s combination of irreplaceable brand power, direct-store-delivery infrastructure, and international scale will restore consistent organic volume growth and protect pricing power against both private-label competition and shifting consumer health preferences.

The framework it prescribed was Economic Moat Analysis. And a moat in packaged food is not the logo on the bag. It is the ability to charge more than the store brand sitting six inches away and keep the customer anyway.

Read that definition again with a $4.56 gas pump in mind. A moat is not tested in good times. In good times everybody’s volume grows. A moat is what is supposed to hold when the shopper is counting. This quarter is not an unfair test of Pepsi’s moat. It is the only kind that means anything.

So the tool did not just tell us to watch Pepsi’s volume. It told us to watch it against everyone standing in the same squeezed aisle.

The control group, and the trap inside it

Here is where it would be easy to cheat, so we will show our work.

The temptation is to line Pepsi’s just-reported quarter against whatever its rivals last posted and declare a winner. That comparison is rigged, and it is rigged against Pepsi. Pepsi’s quarter ran through June 13, so it swallowed the late-May gas spike. Coca-Cola’s last quarter closed April 3. The snack data closes March 29. No peer lived through the worst weeks Pepsi lived through.

So throw it out, and use the window where everybody’s numbers overlap.

The Gap Opened Before the Gas Spike. Year-over-year change, U.S. market, matched periods, spring 2026.

Every bar above ends within two weeks of the others. No gas spike in any of them. The gap is already open.

Coca-Cola grew North America volume 4 percent. Pepsi’s beverage volume fell 2.5 percent in the same weeks. Volume against volume, one country, one shopper, six and a half points apart. That is the cleanest comparison in this story, and Pepsi loses it before the macro arrives.

On the snack side, Utz reported in its 10-Q that U.S. salty snack retail sales rose 2.4 percent in the thirteen weeks ended March 29, citing Circana, while Utz’s own sales rose 4.6 percent. Frito-Lay’s volume grew 2 percent. It grew. It just grew slower than the category it defines, and less than half as fast as a rival a fraction of its size.

And the store brand held. Private label runs about 24 percent of U.S. grocery units, and in FMI’s 2026 work, 17 percent of shoppers cut back on national brands against only 4 percent who cut back on store brands.

Now bring the gas spike back in. In the quarter that followed, Frito-Lay volume slid from plus 2 percent to flat, and beverages from minus 2.5 to minus 4. The macro got harder and Pepsi got worse. Some of that is the shopper, and we will not pretend otherwise.

But the trend was already pointing down before the pump did anything, and that is what a macro excuse cannot reach backward and explain.

A control group only works if you name the leaks. Utz and the category report retail dollars; Coke and Pepsi report volume. Coke conceded it was lapping an easy comparison. And no peer has yet reported the gas-spike quarter Pepsi just did.

That last leak is why this piece has a sequel.

The asterisks we published, graded

In June we flagged three ways this recovery might fool us.

Asterisk one, the volume may be bought with promotion. This came back worse than we wrote it. We expected volume propped up by discounts. What arrived was discounts that failed to prop it up at all. Prices down as much as 15 percent, food volume flat, beverages down 4 percent, and last quarter’s 2 percent snack gain did not repeat. A brand buying its customers back is at least buying something. Broke.

Asterisk two, the growth may be acquired. Pending, and Pepsi kept it that way. The release did not break out beverage organic growth excluding CELSIUS and poppi. Last quarter’s split was telling: 9 percent reported growth, roughly 2 points organic. We will read the 10-Q and report the number.

Asterisk three, the margin may be borrowed. Also pending, and the hedges are the clock. Management has said they run six to twelve months, and the Iran-related cost impact was still to be determined.

The story the release told, and the number that broke it

Watch how a quarter gets dressed. Net income came in at $2.98 billion, up from $1.26 billion. More than doubled. Revenue rose 6.4 percent to $24.18 billion, beating estimates.

Except profit did not double because the business improved. It doubled because last year’s quarter carried a $1.86 billion non-cash impairment charge. Lap a bad year and you look like a hero. Strip that and adjusted earnings were $2.20 per share against the $2.21 expected. A miss.

The revenue beat was real but not American. Global food volume rose 3 percent, and that growth came from overseas.

None of it is hidden. It is all in the release. But you only go looking if something told you which number was load-bearing.

The test that settles it, and its date

We do not tell you to buy Pepsi or sell it. We tell you whether the assumption its price rests on has earned your conviction. It has not. The moat test needs volume rising while price holds. Pepsi delivered price falling and volume flat, and it was already trailing the aisle before the macro turned. Classification stays Watch.

Now the falsifiable part, written before the number exists. Coca-Cola reports its second quarter on July 28, covering roughly the weeks Pepsi just covered, including the gas spike. That is the clean overlay we lack today.

If Coke’s North America volume also goes negative, the economy did this, our read was too hard on Pepsi, and we will say so in print. If Coke’s volume holds while Pepsi’s fell 4 percent, the macro excuse is finished, and what’s left is share loss.

Two paths. One date. We will be here either way.

Keep this after the quarter is filed

Here’s the lens worth stealing. When a company blames the economy, go find the control group.

Every management team facing a bad quarter reaches for the same explanation, and sometimes it’s true. The economy really is squeezing the American shopper. But an excuse that applies to everyone is testable against everyone. Find the competitor selling to the same customer, in the same aisle, in the same weeks. If they grew and this company didn’t, the economy was the setting, not the cause.

Pepsi still owns one of the great distribution machines in the world. Whether the brands riding on top of it can still charge for being the brands is the open question, and on July 28 a company in Atlanta answers a large part of it.

We have posted our pre-registered test for Coca-Cola’s July 28 print. It names, before the number exists, the result that would prove this read wrong. Subscribers can read it, along with the Firewall card and the source data behind the chart, in the Working Papers at readthelongview.com.

Not investment advice. The subscriber decides.