Market Structure vs. Competitive Dynamics: When the First Layer Is True

Some investing mistakes are easy to explain afterward.

The business was weak. The balance sheet was stretched. The growth was low quality. The valuation was absurd. In those cases, the lesson is usually obvious, even if it was painful.

The harder mistakes are different, and they usually begin with something reasonable.

SAP does have sticky enterprise customers. Coca-Cola does have one of the great consumer brands. Monday.com has shown real growth. Palantir sits in the middle of a powerful conversation around data, AI, and enterprise decision-making.

None of that has to be false for the analysis to go wrong.

That is the point.

The first layer of a thesis can be true and still not be enough.

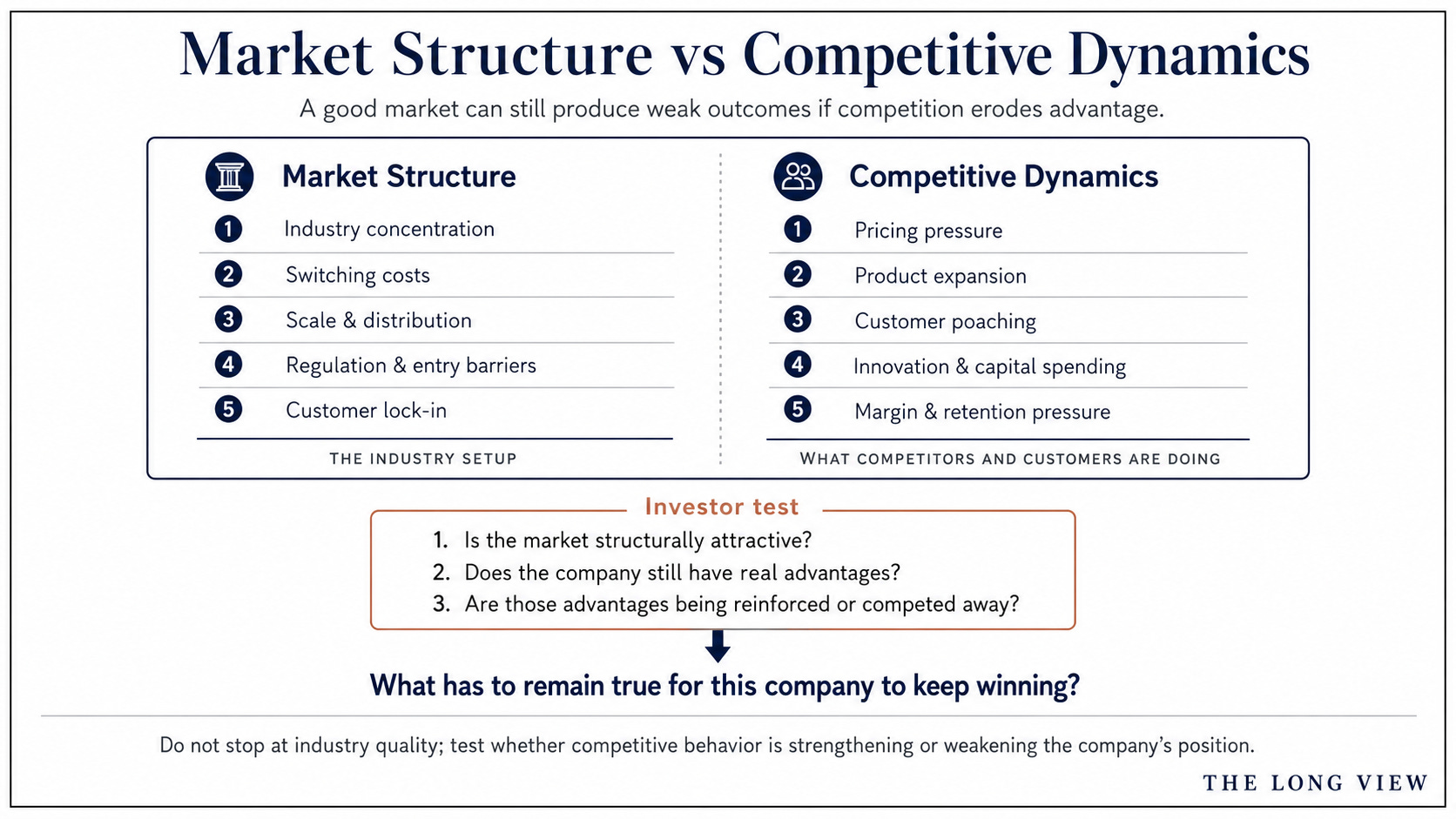

This week’s framework, Market Structure vs. Competitive Dynamics, is useful because it pushes past that first layer. It does not ask only whether a company has visible strengths. Most good companies do. It asks whether the market still reinforces those strengths in the same way.

That is a harder question.

It is also the question investors tend to ask too late.

A moat is not just something a company owns. It is a relationship between the business and the market around it. Customers, competitors, distribution, technology, regulation, habits, pricing power, switching costs — all of these shape whether an advantage keeps working.

When that relationship changes, the company may still look strong for a while.

That is what makes the mistake dangerous.

The old evidence does not disappear immediately. The customer base may remain. The brand may still be recognized. Revenue may continue growing. The story may still sound right. But the next layer of proof may be weaker than the last one.

That is where investors have to pay attention.

Not just to the company.

To what the company depends on.

The problem with stopping at “good business”

“Good business” is a useful starting point. It is a bad stopping point.

Once investors attach that label, the label can start doing too much work. It becomes shorthand for durability, and durability is exactly what still has to be tested.

The question is not simply whether SAP has switching costs, whether Coca-Cola has brand power, whether Monday.com is growing, or whether Palantir has a compelling position in an important market.

The better question is what has to remain true for those strengths to keep mattering.

For SAP, the issue is not whether the installed base exists. It does. The issue is whether that installed base still pulls future spending toward SAP as enterprise software moves deeper into cloud architecture, data integration, workflow flexibility, and platform competition.

For Coca-Cola, the issue is not whether the brand is famous. It is. The issue is whether consumer behavior keeps reinforcing that brand with enough strength to support volume, pricing, shelf space, and habit over time.

For Monday.com, the issue is not whether the company has grown. It has. The issue is whether growth is making the business more defensible, or whether it is simply happening inside a category that attracts more competition.

For Palantir, the issue is not whether the story is interesting. It clearly is. The issue is whether the market structure has matured enough to prove the level of dominance investors may already be assigning to it.

That is the difference between admiring a company and underwriting an advantage.

One is easier, the other is more useful.

When the customer stays but the future moves

SAP is a good reminder that retention can be comforting without being complete.

In enterprise software, customers do not casually replace core systems. The costs are high, the risk is real, and the operational disruption can be enormous. That kind of embedded position matters. It can protect a business for a long time.

But protection is not the same as momentum.

A customer can stay because leaving is painful while directing the next layer of spending somewhere else. That is a subtle distinction, but it is an important one. It means the installed base can remain intact even as the competitive center of gravity begins to shift.

That type of change does not always show up first as churn. It may show up in where new workloads go, where cloud decisions are made, where customers want more flexibility, or where adjacent platforms begin to capture incremental budget.

The mistake is looking only at whether customers leave.

The better signal may be where they choose to spend next.

That question matters because the next dollar often tells you more about the direction of the moat than the last contract.

When a brand is remembered more than reinforced

Coca-Cola teaches a slower version of the same problem.

There is no need to force a weak-company argument here. Coca-Cola is not weak. The brand, distribution system, and history of consumer habit are real advantages.

But even great brands have to keep being reinforced.

Recognition is not the same as behavior. People can know a brand, respect a brand, even feel attached to a brand, while making different choices at the margin. In consumer businesses, those marginal choices matter because the moat is built through repetition: the purchase, the occasion, the shelf space, the pricing decision, the habit formed again and again.

The risk is not that Coca-Cola suddenly becomes irrelevant. That is too crude.

The more useful question is whether the behaviors that made the brand so powerful continue to work with the same force. If younger consumers form different habits, if alternatives improve, if volume becomes harder and pricing carries more of the burden, the moat can weaken while the brand still looks dominant.

That is why slow erosion is hard to analyze.

Nothing dramatic has to happen.

The company can remain profitable. The brand can remain famous. The investor can keep pointing to the same strengths that made the business exceptional in the past.

But the market may already be asking whether those strengths are still being renewed.

When growth makes the thesis feel finished

Growth is dangerous because it can make an unfinished thesis feel complete.

With a company like Monday.com, the first layer is easy to see. The business has grown, the category has expanded, and customers are clearly looking for better ways to manage work, collaboration, and workflows.

That is meaningful.

It is not conclusive.

A company can grow because it is building a durable competitive position. It can also grow because the market is young, buyers are experimenting, budgets are available, and the category has not yet settled.

Those are very different situations.

The question is whether growth is changing the competitive position of the business. Is the product becoming more embedded? Are customers expanding usage because the software is becoming more necessary? Is the company gaining advantages that make it harder to replace? Or is the growth simply making the market more attractive to larger platforms, specialized competitors, and new entrants?

That is the test.

Revenue growth tells you the company is getting bigger.

It does not, by itself, tell you whether the company is becoming harder to compete with.

For long-term investors, that difference matters more than the growth rate alone.

When the story moves faster than the structure

Palantir is the case where the narrative can do the most damage if the investor lets it.

That does not mean the narrative is empty. It means the narrative is powerful. Data, AI, government relationships, commercial expansion, and mission-critical software are not small themes. They are exactly the kind of themes investors pay attention to because they feel tied to the future.

The risk is that a strong story can create a feeling of certainty before the market structure has earned it.

In emerging markets, the rules are still forming. Customers are still learning what they need. Competitors are still adjusting. Use cases are still developing. The economics of the category are still being shaped.

That does not make Palantir uninteresting.

It makes the burden of proof higher.

The investor has to ask whether current leadership is becoming structural advantage. Are customers becoming more dependent? Are switching costs increasing? Is differentiation becoming clearer? Is the company’s role becoming more necessary as the market matures?

A narrative can tell you where to look.

It cannot do the underwriting.

At some point, the story has to become structure.

Until then, the investor should be careful about treating possibility as proof.

The common mistake

The four companies are different on purpose.

SAP is about customer captivity and future spending. Coca-Cola is about brand memory and behavioral reinforcement. Monday.com is about growth and defensibility. Palantir is about narrative and structural proof.

Different markets. Different risks. Same investor habit.

We find a real strength, then we let it carry more weight than it should.

That is not the same as being careless. In some ways, it is more dangerous because the original observation is often correct. The company really does have something attractive. The problem is that the attractive thing may not answer the most important question.

What keeps it working?

That is the question this framework is trying to force.

Not what made the company strong.

What keeps the strength relevant.

That distinction is small enough to miss and large enough to matter.

What to watch before the numbers show it

The financial statements often confirm competitive change after the market has already started to sense it.

By the time margins compress, revenue slows, churn rises, or growth becomes more expensive, the argument may have already changed. The earlier evidence is usually less obvious. It shows up in behavior.

Where is new spending going?

Are customers choosing the company again, or merely staying because switching is painful?

Is the brand shaping new habits, or mostly benefiting from old ones?

Is growth making the business more defensible, or attracting more competition?

Is the story gaining evidence, or only gaining believers?

None of these questions gives a perfect answer. Investing does not work that way.

But they move the analysis to the right place. They force the investor to study the conditions around the advantage instead of only admiring the advantage itself.

That is the practical value of Market Structure vs. Competitive Dynamics.

It is not a prediction tool.

It is a discipline tool.

It keeps the investor honest when the company still looks strong.

The Long View takeaway

The market does not owe a company future returns because it has been strong in the past.

Strength has to keep earning its position.

A sticky software business still has to win future spending. A famous brand still has to shape future behavior. A growth company still has to turn scale into defensibility. A powerful narrative still has to become structural proof.

The investor’s job is not to admire the moat.

The job is to keep testing what reinforces it.

That is the better habit.

Not asking only:

Is this a good company?

But asking:

What has to remain true for this company to remain a good investment?

Those are different questions.

The first one can make you comfortable.

The second one keeps you honest.

And in investing, honest analysis matters most before anything looks broken.

Strength is not static.

It has to be re-earned as the market changes.

Postscript

For readers who want the deeper company-level breakdown, this week’s Long View Institutional Review focuses on SAP.

That review goes further into SAP’s enterprise software position, the cloud transition, customer stickiness, and whether the company’s historical advantage still fits the market structure forming now.

The companion Price / Value piece asks the next question:

Is the current price reflecting durable advantage, or assuming more stability than the structure supports?

This distinction between owning an advantage and having the market continuously reinforce that advantage is incredibly important.

One thing this framework made me think about: in commerce specifically, many platforms may have unintentionally weakened their own long-term economics by reinforcing visibility competition instead of demand coordination.

The strongest line for me was:

“The next dollar often tells you more about the direction of the moat than the last contract.”

That feels directionally true far beyond enterprise software.