Margin of Safety is not just buying cheap

Why the real work is deciding whether price leaves enough room for error.

Framework: Margin of Safety

Category: Frameworks

Core Question: What does a real valuation buffer look like across different kinds of businesses?

Objective: To help readers understand that margin of safety is not a low-multiple rule, but a discipline for judging whether price leaves enough room for uncertainty and error.

Opening Frame

Margin of safety is one of the most famous phrases in investing, and one of the most casually misused.

In everyday discussion, it is often reduced to a simple instruction: buy with a discount. But that version is too shallow to be very useful. Plenty of stocks trade at low multiples without offering meaningful protection. Plenty of strong companies deserve premium valuations without becoming untouchable. The real work is not identifying what looks cheap. The real work is deciding whether the price leaves enough room for the business to be less than perfect and still justify the investment.

That is why this framework matters.

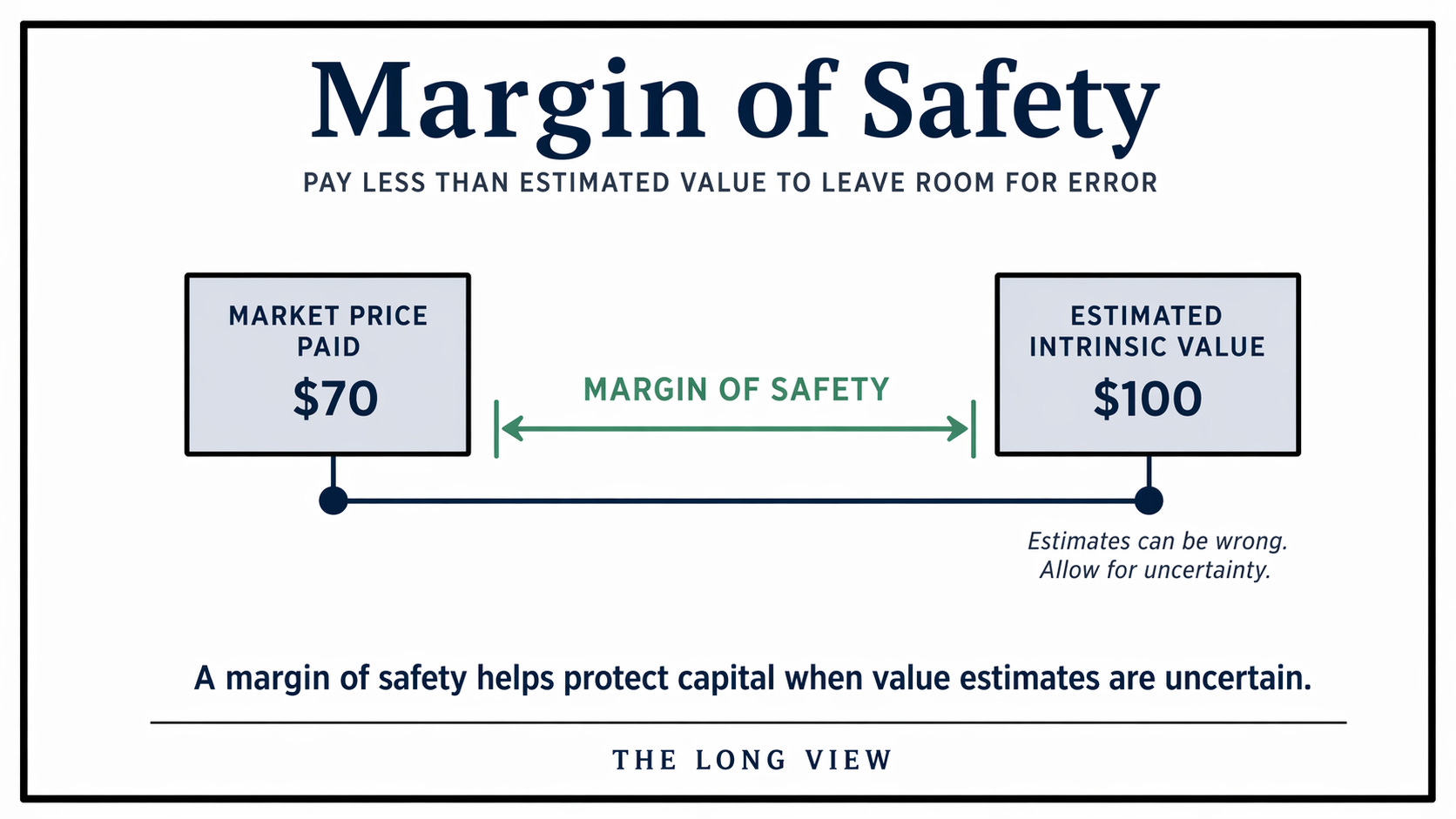

Valuation is never an act of certainty. It is an estimate built on assumptions about growth, margins, reinvestment, competition, capital allocation, cyclicality, and duration. The margin of safety is the buffer between those assumptions and the price paid. Its purpose is not to make investing risk-free. Its purpose is to reduce the damage when reality is less favorable than the investor expected.

Core Distinction

Margin of safety is not a synonym for a low multiple.

A low multiple can reflect fragility, governance problems, cyclicality, or market skepticism that may be entirely justified. A high multiple can reflect business quality that is real, but still not sufficient to protect the investor if the entry price assumes too much perfection.

The framework only becomes useful when it forces the investor to ask a more disciplined question: what kind of error is the current price absorbing, and how much room remains if that error proves larger than expected?

Company Set

This week’s four-company set makes that distinction visible.

Novo Nordisk shows how a premium franchise can still leave little room for disappointment when investors have become accustomed to unusually strong growth and execution.

Alibaba shows the opposite problem. A discounted price may look like protection, but the market may be expressing uncertainty that is not easy to neutralize with a simple valuation discount.

Canadian National Railway shows how durable businesses can tempt investors into paying too much for predictability. The franchise may be strong, but valuation discipline still matters.

Siemens shows how diversified industrial quality can create resilience without automatically creating a true buffer against paying an optimistic price.

Strongest vs Weakest Fit

The strongest fit for the framework this week is Canadian National Railway.

Not because it is automatically the best investment, and not because it must be the cheapest, but because it isolates the core educational question cleanly. The business is durable enough that the reader can focus on the relationship between business quality and entry price without getting lost in a large number of structural unknowns.

The weakest fit is Alibaba, but only in the sense that the framework becomes harder to apply with precision when the investor must incorporate larger confidence discounts. That does not make the exercise less valuable. In fact, it is a useful reminder that a margin of safety is only as credible as the assumptions used to define value in the first place.

Portable Lesson

The portable lesson is this: margin of safety is not a style label. It is a discipline of humility.

It begins with the recognition that the investor’s estimate of intrinsic value is not a fact. It is a judgment. The more uncertain the judgment, the larger the buffer should be. The more obvious and admired the business, the more carefully the investor should inspect whether the price already assumes too much.

Evaluation Checklist

A useful evaluation checklist looks like this:

1. What is my estimate of intrinsic value actually based on?

Is it driven by durable cash generation, asset quality, network strength, or optimistic growth assumptions?

2. What can go wrong without breaking the business?

Could growth slow, margins compress, the cycle weaken, or sentiment normalize?

3. What kind of uncertainty is present?

Operational uncertainty, competitive uncertainty, governance uncertainty, and cyclicality do not deserve the same treatment.

4. How much of the good news is already priced in?

A strong business can still offer a poor setup when optimism is expensive.

5. If I am wrong, how protected am I by the entry price?

That is the real margin-of-safety question.

Long View Closing

The Long View closing is simple. Do not ask only whether a business is good. Do not ask only whether a multiple is low. Ask whether the price gives you enough room to be imperfect. That is where margin of safety begins.

Postscript: This week’s Canadian National Railway entry has been added to the Long View Review System archive. Paid subscribers can access the full archive on The Long View Substack.