Framework: Free Cash Flow Quality

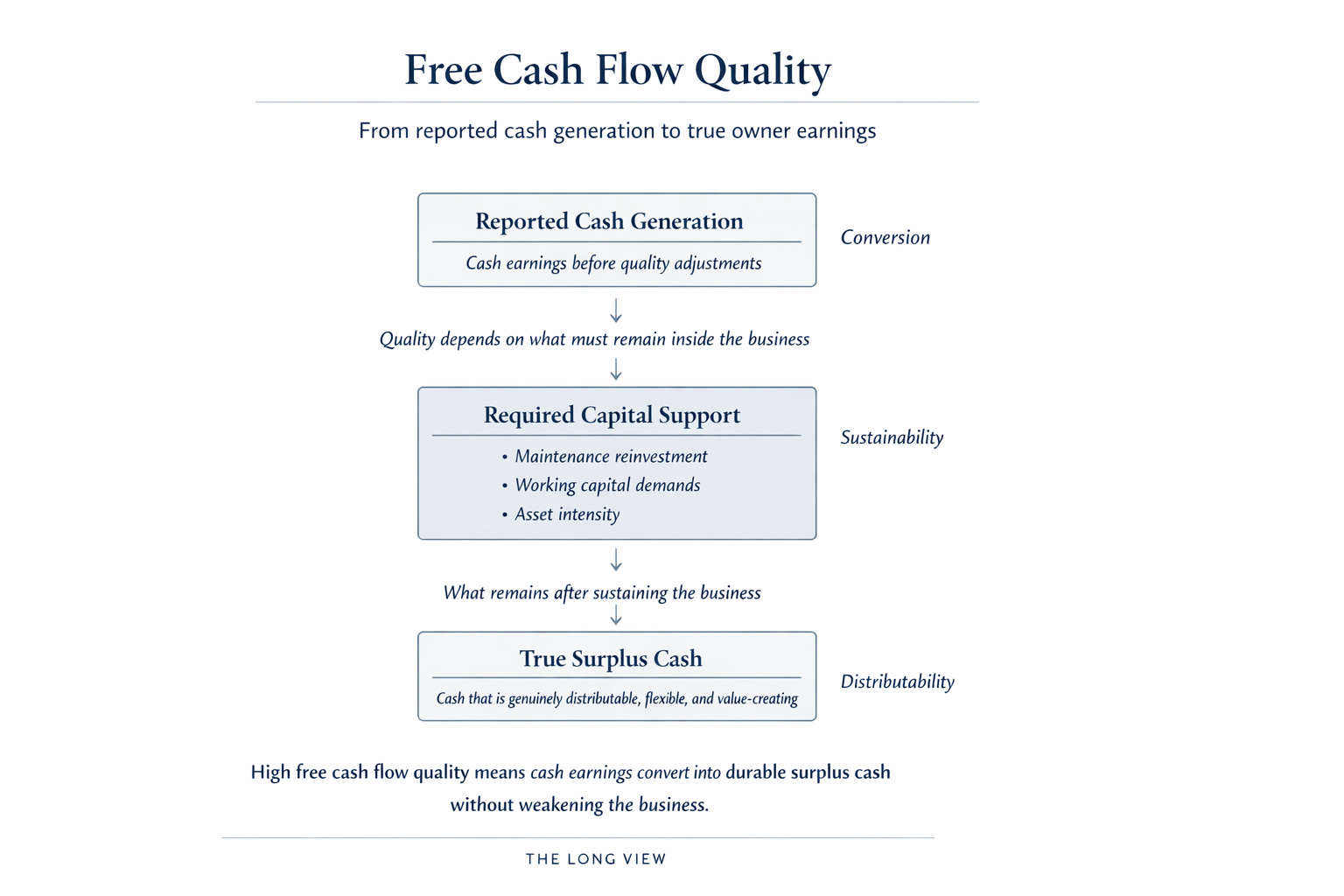

Free cash flow quality is one of the clearest ways to separate accounting strength from economic strength.

Many businesses produce earnings. Many produce cash. Far fewer convert those earnings into durable, flexible, surplus cash that can be reinvested or returned without weakening the business.

This week’s set shows why the framework matters. Brookfield Renewable appears strong at first glance because its assets generate visible, durable cash flows. But infrastructure ownership comes with persistent reinvestment needs. That makes Brookfield Renewable a useful reminder that stable cash generation and high-quality free cash flow are not automatically the same thing.

Canada Goose highlights a different issue. The company benefits from premium positioning and strong brand economics. But free cash flow quality does not follow from margin strength alone. Inventory timing, seasonal demand, and working capital execution all shape whether earnings become usable cash. In this framework, Canada Goose is a moderate-fit business because the economics are attractive, but the cash conversion is not fully clean.

AutoZone is the clearest strong-fit case in the group. Its operating model converts steady demand into excess cash with unusual consistency. The reinvestment burden is manageable, the cash conversion is strong, and management has a long record of deploying that cash with discipline. This is what strong free cash flow quality looks like: reliable conversion, limited drag, and flexible excess cash.

Bank Central Asia extends the framework into financials. Here, cash flow quality is less about inventory or capital expenditure and more about funding structure. A durable low-cost deposit base supports stable earnings and capital generation. That makes Bank Central Asia a strong analog for cash flow quality in a banking context.

The dispersion across the set is the real lesson. Brookfield Renewable shows that visible cash flows can still be moderated by capital intensity. Canada Goose shows that strong brand economics do not guarantee clean cash conversion. AutoZone shows how operational discipline can produce durable excess cash. Bank Central Asia shows that in financials, funding structure can serve as the foundation of cash flow quality.

Strongest vs weakest fits

The strongest fits this week are AutoZone and Bank Central Asia because both models leave more of their cash generation flexible after the business supports itself. The weaker fits are Brookfield Renewable and Canada Goose, though for different reasons: one is constrained by capital intensity, the other by conversion variability.

Evaluation checklist

How much cash remains after the business supports itself?

How stable is cash generation across environments?

How much reinvestment is required to preserve the model?

How efficiently is excess cash allocated?

Is the cash generation structural or temporary?

Long View research is designed to help investors evaluate businesses through durable frameworks rather than short-term narratives. Our institutional reviews emphasize structure, discipline, and capital efficiency as the foundations of long-term outcomes.