Core question: What determines whether business pressure becomes temporary weakness or permanent damage?

Objective: Help readers understand downside as a structural path, not a price movement.

Most investors misunderstand downside

Most investors think downside is about how far a stock can fall. It isn’t. Two businesses can decline the same amount and carry completely different risks. The difference is not in the price. It’s in what has to happen next for the business to recover.

Most investors notice downside when the price falls. That’s understandable. It’s also where most of the useful information is already gone. A declining price tells you something has changed in the market’s view. It does not tell you whether the business itself is becoming weaker, whether the pressure is temporary, or whether the system can recover without outside help. That is the distinction that matters.

Downside is about dependency after pressure appears

Downside Asymmetry is not about whether a business can decline. Every business can decline. It is about what happens after pressure appears. Does the business absorb the pressure and continue operating with control? Or does it become more dependent on conditions improving? That is where the difference shows up.

How it shows up across four businesses

Nu Holdings

Nu Holdings is the clearest example of dependency in this week’s set. On the surface, Nu looks like a strong growth story. Customer expansion, product adoption, and operating scale all move in the same direction when conditions are favorable. But growth does not create independence on its own. If a business relies on continued expansion, funding access, and stable credit conditions, then downside is not just slower growth. It is reduced flexibility. That is a different type of risk.

Samsung

Samsung shows a different pattern. Its earnings move with cycles. Demand weakens, pricing adjusts, margins compress, and results deteriorate. But cyclical pressure is not automatically structural damage. If the business retains scale, internal funding, and operating capacity, then the decline can be absorbed. Volatility and fragility are not the same thing.

Unilever

Unilever sits on the other end of the spectrum. It is not the most dynamic company in the group, and that is part of the lesson. Businesses built on repeat demand do not need rapid growth to remain stable. Consumers may adjust behavior, but the underlying need does not disappear in the same way it can elsewhere. That gives the business time.

JD.com

JD.com introduces a different kind of risk. Its downside does not sit in one place. Demand, competition, pricing, and execution all interact. Each pressure point may be manageable on its own. The difficulty comes when they move together. When pressure spreads across multiple parts of the business, flexibility can narrow quickly.

The takeaway

The lesson across all four is straightforward. Downside is not one thing. It depends on what the business needs in order to keep functioning.

· Nu needs supportive conditions.

· Samsung needs the cycle to improve.

· Unilever needs demand to remain stable.

· JD needs multiple pressures to stop compounding.

Those are not interchangeable.

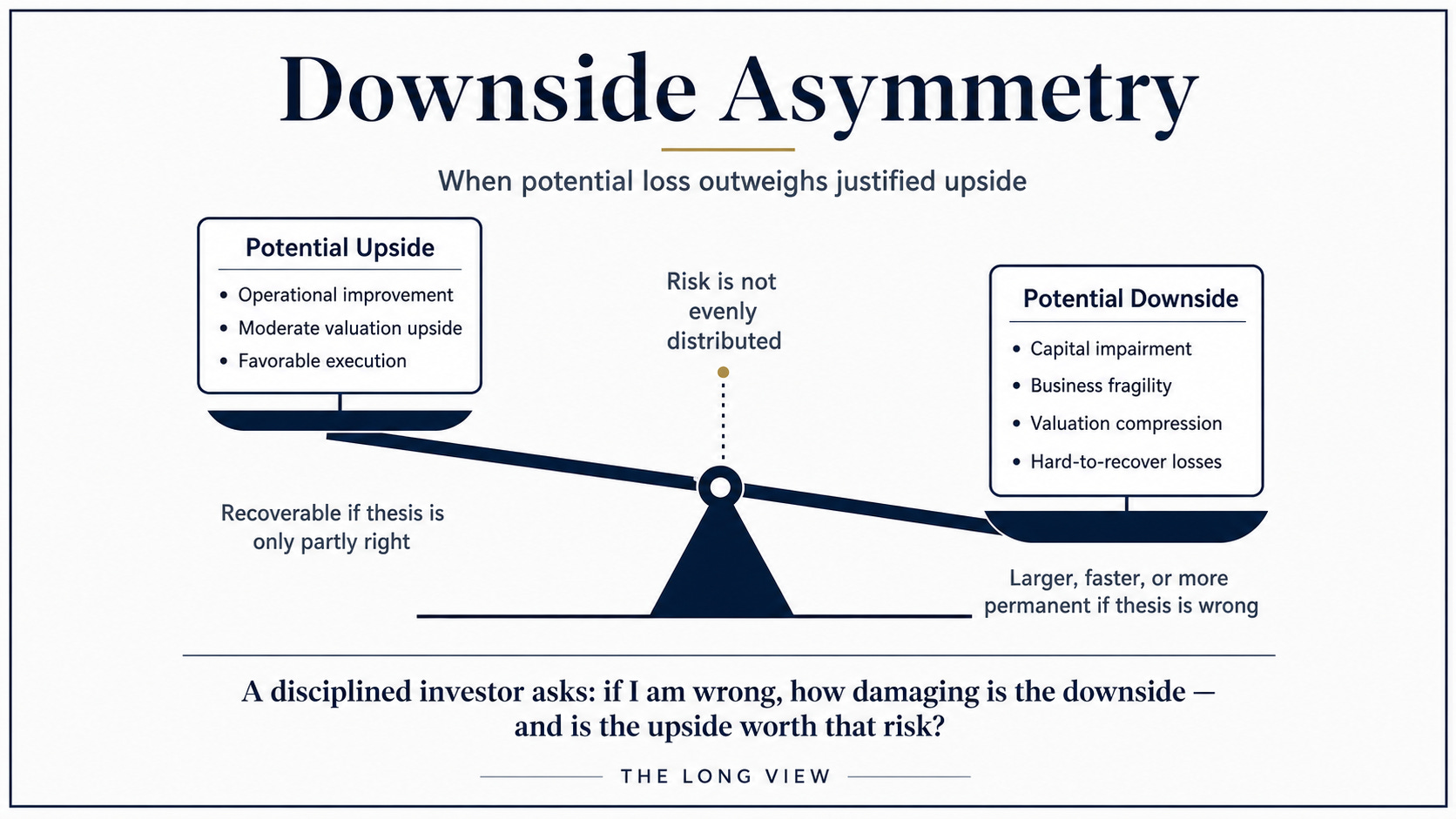

For investors, the practical question is simple: What has to go right for this business to recover? If the answer depends mostly on the business itself, the downside is often contained. If the answer depends on several external conditions improving at the same time, the downside is harder to control.

The market shows you the decline first. Understanding the structure tells you what comes next.

Postscript

For readers who want the full company-level breakdown, this week’s Long View Institutional Review on Nu Holdings—along with the companion Price/Value analysis—is available inside the Review System archive.