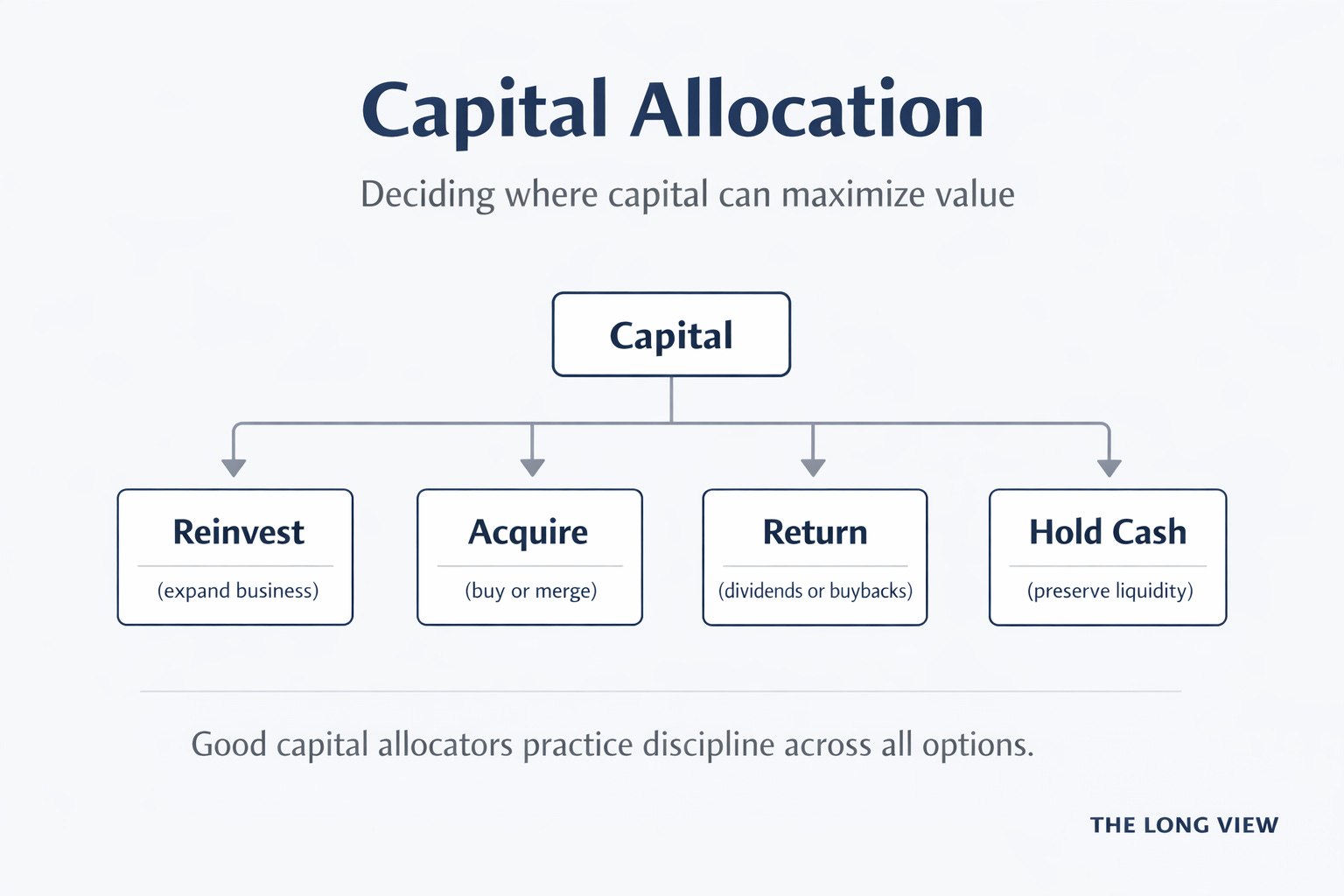

Capital allocation is one of the most important subjects in investing because it sits upstream of almost everything else. A business can have strong products, loyal customers, and a durable position, yet still produce mediocre outcomes if management deploys capital poorly. Over long periods, the market tends to reward not just what a business is, but what it chooses to do with the cash it produces.

Professional investors usually start with a simple question: where is the next dollar best deployed? That dollar can be reinvested in the business, used to acquire another business, returned to shareholders, or held for future opportunity. The right answer changes over time, and the discipline to admit that change is often the edge.

This week’s case studies illustrate four distinct allocation profiles. Apple represents a mature cash generator with limited high-return reinvestment capacity at scale. In that situation, activity is not the goal—restraint is. Buybacks and dividends can be sensible when they prevent forced reinvestment into marginal projects, but only when executed with valuation awareness and long-term discipline.

Microsoft shows a different profile: a business with meaningful reinvestment runways, alongside the option to use acquisitions to extend platforms. The institutional view is not that acquisitions are good or bad in the abstract, but that they must extend durable capabilities rather than substitute for organic strength. Reinvestment remains primary when incremental returns remain attractive; buybacks are secondary to opportunity.

Berkshire Hathaway highlights the role of patience. Holding cash is not a failure of imagination—it can be a strategic decision when opportunity is scarce. Forced allocation is where many long-term mistakes occur. Selective deployment, combined with opportunistic buybacks when valuation is favorable, is an approach built to preserve optionality and avoid permanent errors.

Costco illustrates allocation through culture. Some of the most durable businesses deploy capital not to maximize short-term margins, but to reinforce trust, scale, and efficiency. Reinvestment that protects loyalty can be more valuable than optimization that boosts near-term profitability. In this model, discipline is expressed through consistency.

A practical way to evaluate capital allocation is to look for three things. First, a clear hierarchy: reinvest when returns are high, return capital when they are not, and hold cash when uncertainty makes deployment unattractive. Second, alignment: incentives and communication that emphasize per-share, long-term outcomes rather than headline expansion. Third, restraint: evidence that management can say no—both to acquisitions that don’t fit and to reinvestment that no longer earns attractive returns.

Capital allocation is not a forecast. It is a repeated decision process. Over time, outcomes tend to follow that process. The Long View is built around frameworks like this because they remain useful regardless of the headlines