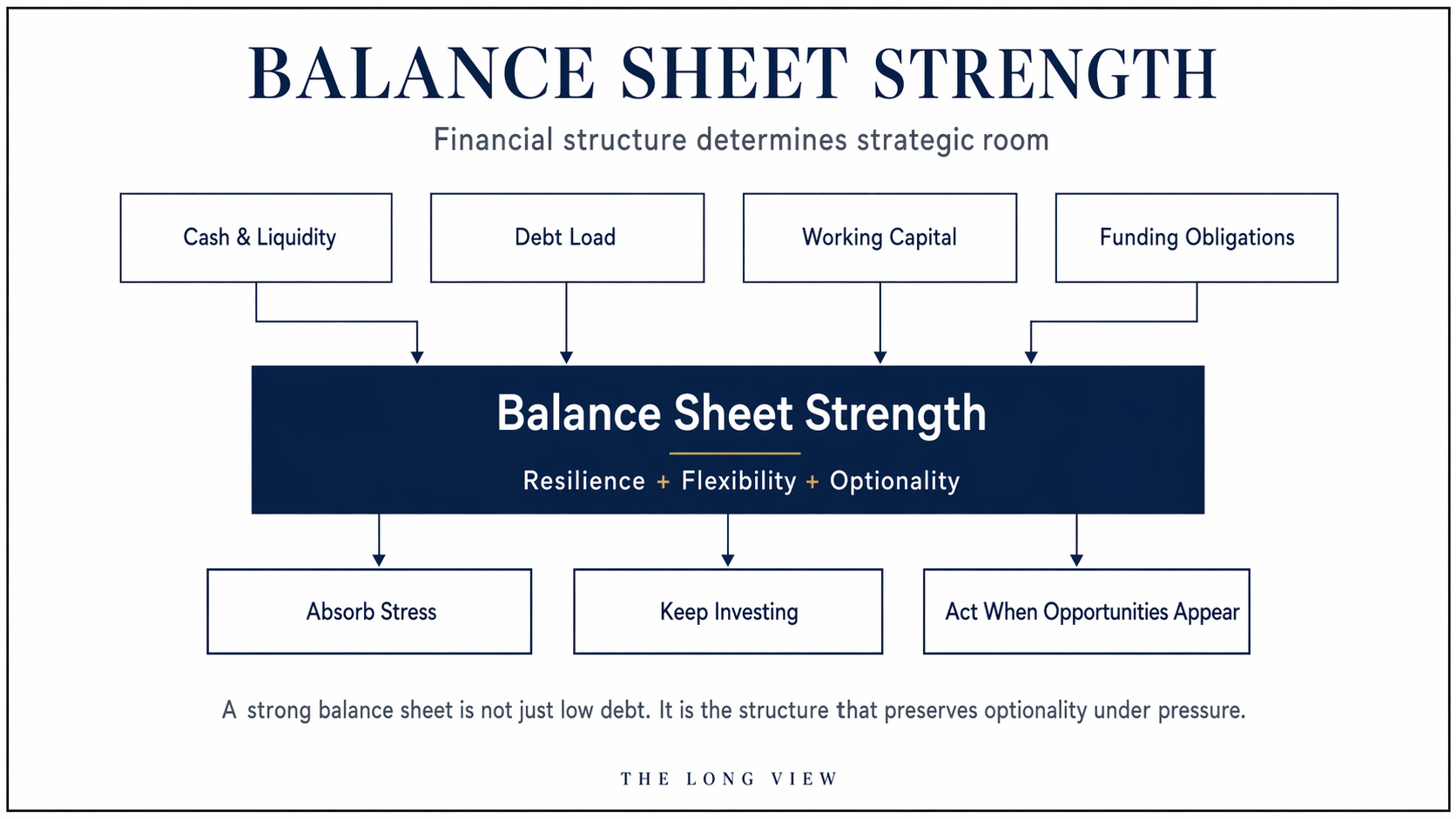

Framework: Balance Sheet Strength

Category: Frameworks

Core Question: What does a balance sheet actually allow management to do?

Objective: Help readers understand balance sheet strength as strategic room, not just low debt.

Most investors read the balance sheet too quickly.

They see cash.

They see debt.

They make a judgment.

Safe. Risky. Strong. Weak.

That is usually too shallow to be useful.

A balance sheet is not just a snapshot of what a company owns and owes. It is a map of what management is still free to do when conditions get harder, when capital needs rise, or when the next opportunity appears.

That is the real subject this week.

Balance Sheet Strength is not the absence of debt. It is the presence of room.

Room to keep investing.

Room to absorb pressure.

Room to avoid forced decisions.

Room to stay rational when weaker businesses lose that luxury.

That distinction matters because the same balance sheet can look comfortable in a headline and demanding in practice.

A company can show a large cash balance and still be carrying a business model that asks more and more from that cash.

Another can spend heavily, carry a busy balance sheet, and still be financially stronger because the operating engine remains well ahead of the demands placed on it.

That is why balance sheet analysis matters. And it is why investors who treat it like a quick cleanliness test usually miss the point.

This week’s company set makes that visible from four different angles: Sea Limited, Moncler, TSMC, and DuPont de Nemours.

Each one shows a different version of the same question:

What is the balance sheet actually funding, protecting, or preserving?

Sea is the most instructive place to start because it shows how easy it is to overread a headline improvement.

At a surface level, Sea looks materially healthier than it did in its earlier, more fragile phase. Liquidity improved. Scale expanded. The business now sits across e-commerce, gaming, and digital financial services. But Sea also ended 2025 with a much larger loans receivable base, which means more of the system’s financial capacity is now tied to a growing credit operation. That changes the burden placed on the balance sheet.

The question is no longer whether Sea has cash.

The question is whether Sea’s liquidity remains comfortably ahead of the financial complexity it now carries.

That is a better question because it forces the investor to stop treating cash as a trophy number.

In Sea’s case, the balance sheet has improved.

But the job of the balance sheet has also become harder.

That is the distinction.

Moncler offers almost the opposite lesson.

This is what balance sheet strength looks like when it expresses itself through restraint rather than rescue.

Moncler does not need an elaborate defense here. The business finished 2025 with a strong net financial position, healthy free cash flow, and enough room to invest while remaining composed. Working capital moved higher, but management tied part of that increase to front-loading key raw materials.

In a luxury business, that matters.

A stronger balance sheet gives management room to protect distribution, preserve brand standards, and avoid reacting to short-term pressure in ways that can weaken the franchise.

TSMC is the sharpest case in the set.

Investors often see enormous capital spending and jump straight to financial risk. That shortcut fails here.

TSMC spent heavily because the model demands massive reinvestment. But heavy spending is not the same as financial weakness. The right question is whether the business can fund that spending comfortably from a position of operating strength.

In 4Q25, TSMC reported very large cash balances, substantial net cash reserves, and a strong current ratio even after heavy capital spending.

That is not a weak balance sheet working too hard.

It is a strong balance sheet doing its job.

DuPont is the messier case, which is exactly why it belongs in the week.

Messy cases are useful because they stop the framework from turning into a slogan.

DuPont’s year has to be read through lower year-end cash, the Electronics separation, portfolio actions, and the question of what flexibility truly remains after the transition.

So the right reading is not simply that the structure may be cleaner.

The right reading is whether the post-separation company now gives the remaining business more durable flexibility than it had before.

Put together, the week leaves a simple lesson.

Balance sheet strength should be judged by what it preserves.

Does it preserve reinvestment?

Does it preserve resilience?

Does it preserve patience?

Does it preserve management’s ability to act from choice instead of constraint?

That is the real work.

Not cash versus debt in isolation.

Not a leverage ratio without context.

Not a quick label.

A balance sheet is strong when it keeps the company from becoming reactive.

That is what Sea is still trying to prove.

That is what Moncler quietly protects.

That is what TSMC most clearly demonstrates.

That is what DuPont is still trying to rebuild through structure.

For readers, the practical checklist is straightforward:

1. How much liquidity is truly available?

Not just reported, but usable.

2. What is the business model asking that liquidity to support?

Growth, credit, inventory, capex, restructuring, or something else.

3. Are debt and obligations manageable relative to cash generation?

Not in theory. In the actual operating reality of the business.

4. Is working capital controlled, or becoming a silent source of pressure?

5. Could management keep investing intelligently if conditions weakened?

6. Is the balance sheet funding offense, absorbing stress, or quietly masking a more demanding structure?

That last question is the one most worth keeping.

Because once you start reading the balance sheet that way, you stop treating it as a static report and start treating it as a source of optionality.

That is the better habit.

And it is usually where better business judgment starts.

Postscript:

For readers who want the full company-level workup, this week’s Long View Institutional Review on Sea Limited — along with the companion Price / Value analysis — is available in the Review System archive for paid subscribers.

Really liked the framing of balance sheet strength as “room” rather than just low debt. The point about working capital quietly shaping flexibility is especially important and often underestimated.